QuickBooks Internal Underwriting Tool

A 0:1 product creation for QuickBooks underwriting team to help alleviate bottleneck constraints.

Summary

Lending grew 2x compared to pre-pandemic levels in FY22, but 60%+ of loan applications still require manual review. This is putting unprecedented strain on the underwriting team, forcing them to work overtime, including weekends and holidays.

It’s a good problem for the business but a bad one for the people who make the business possible. We’re expecting originations to double in the next fiscal year. This just isn’t feasible with the current tools and auto-decisioning rates. The “bottleneck” will become a “wall” unless we solve this problem.

Our team ventured on a work track to discover the shortcomings of our current underwriting system and identify how we can help.

Problems

Business:

Receiving more applications than can process within our 2-day service-level agreement.

Can’t hire or train fast enough – hiring, training, and ramping up can take several months.

Two main scaling challenges:

Internally: the average time it takes an underwriter to pick up an application ranges between 2 and 8 days.

Externally: Time To Decision for manually reviewed apps averaged 8.9 days (time between when a customer submits an app and receives a decision + delays/wait times).

Customers:

Long wait times.

Frequent document requests.

Understanding

To kick things off, our team needed to understand the entire underwriting workflow in order to decide where we could step in and help. We spent a month deep diving into what it's like to be an underwriter at QuickBooks. Our team performed a number of different activities to help grow our knowledge.

Mapping Out the Underwriting E2E Journey

Once our team understood everything that underwriters were doing daily, we could narrow down some possible areas of their process we felt could be enhanced. We spent a few weeks reviewing existing documents and performing follow-me-home interviews with our underwriting team and were able to create a high-level E2E of the underwriting experience with the insights we gained.

Financial Reviews

Our team identified the financial review portion of the underwriting work stream as the area we could create the biggest impact and solve those larger scaling issues discussed earlier.

Background

~30% of all applications Lending receives require an underwriter to review 12 months of bank transaction data. We call this part of the underwriting process the “Financial Review.”

The Financial Review is the most manual and time-consuming stage of the Underwriting process. The process can take anywhere from a few minutes to an hour depending on the complexity of the business transactions and the tenure of the underwriter. The average time to complete a financial review as of this writing is 20 minutes.

The goal of the financial review is to assess the cash flow and financial health of a borrower so that we can make an informed risk-based decision.

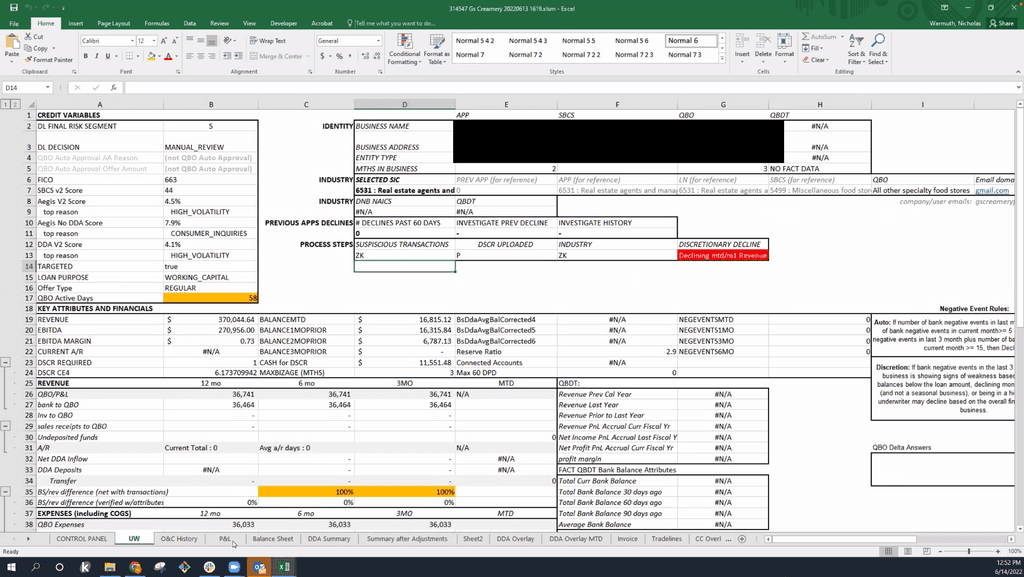

The Excel Checklist

Whenever an application requires manual financial review, an Excel spreadsheet of the customer’s financial and personal data is created (our underwriting team refers to this as the “Checklist”).

The purpose of the Checklist is to source and present as much financial data as possible for the underwriter to review. This gives the underwriter as holistic a profile of the customer as possible, which in turn allows the underwriter to make an informed decision on whether we should lend to the customer.

You can think of the Excel Checklist as essentially an underwriting financial review tool Lending has built over the years out of necessity.

Goal

Create an internal financial review tool that will allow our underwriting team to ditch that excel checklist. By creating an internal tool we'll allow our data modeling to track what underwriters are doing and learn from them. Over time we'll be able to surface less of what underwriters need to review, because of this data modeling.

Dissecting Excel

Once we landed on getting the underwriting team out of excel and into their own dedicated tool to perform financial reviews, we needed to take a deep dive into the excel spreadsheets they were using. The excel sheet contained over 1000 data points that underwriters were able to review. We met with underwriting, policy, and compliance to understand what each data point referenced and its importance. After 4 discussions a card sorting exercise, and 3 prototyping sessions, it became clear which parts of excel were most important and frequently used by underwriters. We were able to create a new list of only the necessary data points for underwriters to review. We were able to go from over 1000 data points within the original excel sheet to less than 100 data points we'd be keeping moving forward.

Principles

Before deep diving into design work, we created a few principles that would guide design decisions and product priorities.

Inspire confidence by easing friction and preventing avoidable errors.

smooth

Show what's needed, where it’s needed, when it’s needed.

Directional

sign a fresh and elegant experience that motivates action.

Energizing

Reduce noise and make frequently-used data points more prominent.

Focused

Design

After several different iterations and user testing sessions, I landed on this 1 page experience that would help our underwriting team perform financial reviews.

Differences

Excel

→ 17 tabs and 1,000+ insights

→ Need new pivot tables, tabs, and conditional formatting to investigate bank data

→ Requires horizontal scrolling

→ Manually creating formulas and highlighting and selecting transactions to adjust

→ Creating Box folders for each customer, then downloading and uploading spreadsheets to Box

→ Downloading and uploading data to/from Excel

→ Siloed data: all UW work and learnings for each business stays in that business’ Excel spreadsheet

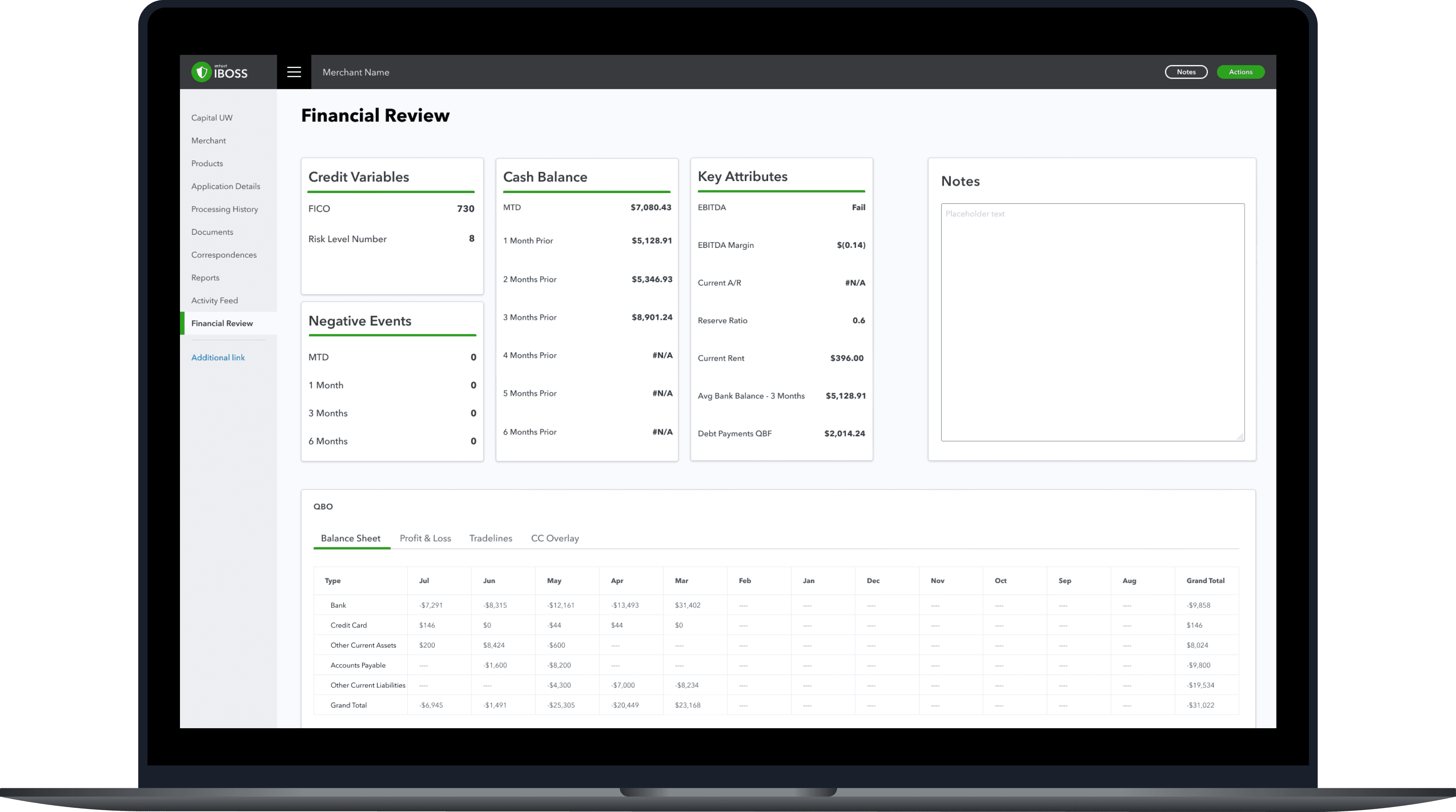

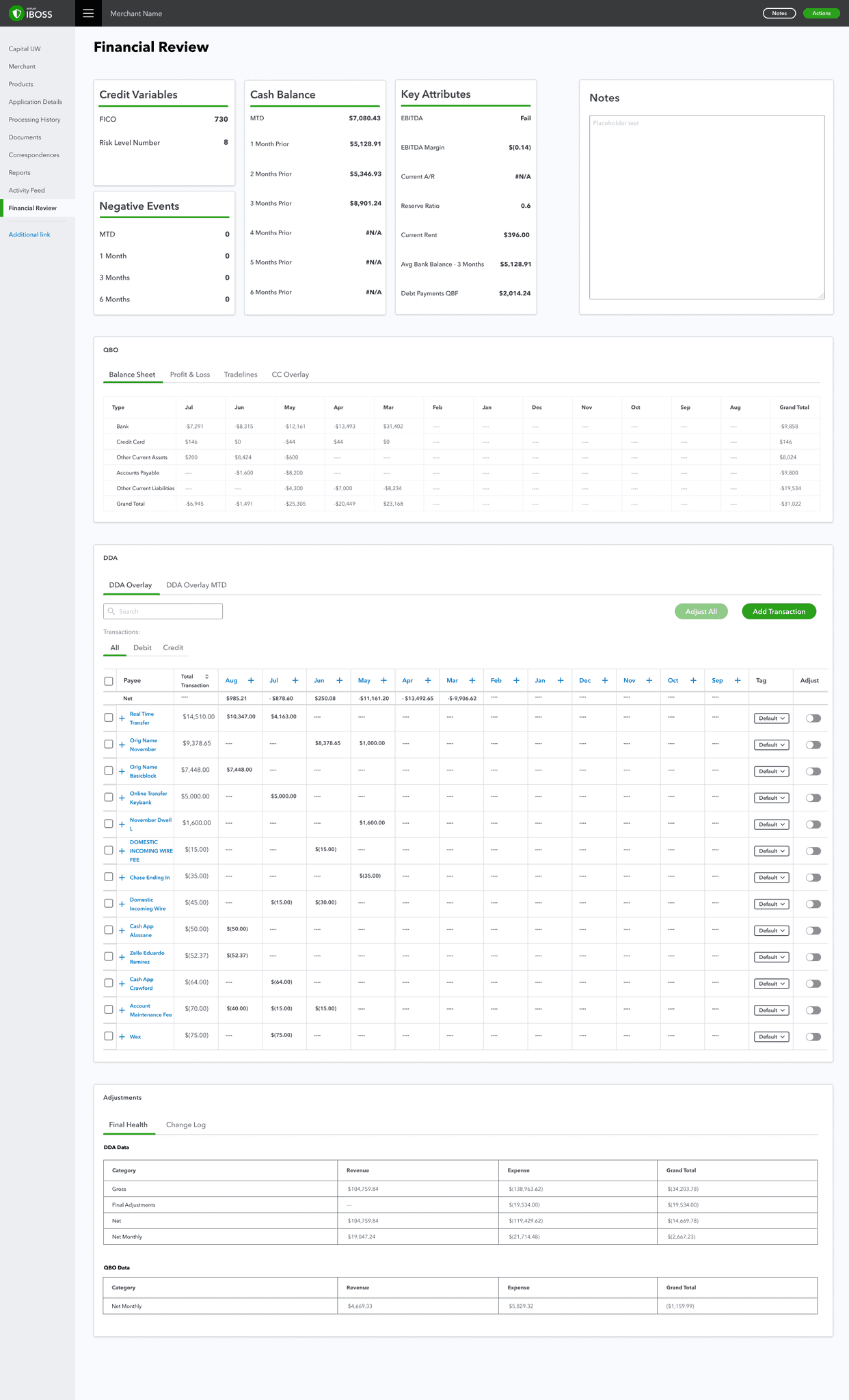

IBOSS

→ 1 page and < 100 of the most critical insights

→ Ability to drill-down within the same experience

→ No horizontal scrolling

→ Remove transactions with a click, all calculations happen automatically

→ No more Box folders or file management required

→ Data is simply available and persisted

→ Connected data: all UW learnings and audits captured and stored in a central place.

Impact

What success looks like

Short-Term Impact

Time to Decision for customers drops

Excel and all of the processes around managing it go away for the Underwriting team

Time to review applications drops

Long-Term Impact

Auto-Decision rates increase

Time to complete Financial Reviews plummets

Underwriting acceleration

Business Benefits

Faster, more accurate reviews

Connected data

Faster training

Customer Benefit

Increased access to Capital

Decreased time to decision and funding